Understanding FinTech

The first step in understanding FinTech is to understand that FinTech is not a new thing. In some form or another, financial companies have always used technology to conduct their business. What has changed, however, (due to technological innovation) is that the financial sector is no longer a “banks only” playground. Instead, it is undergoing significant change and disruption caused by new players — startups, new technologies, and new business models.

Having worked in FinTech with both startups and banks, we’ve put together a beginner’s guide to understanding FinTech. As with every guide, it is definitely not conclusive, nor is the categorisation absolute, but it does give you a good overview of what’s happening, why FinTech matters so much that everyone is talking about it, and why understanding FinTech is important.

Let’s begin, and get to grips with understanding FinTech.

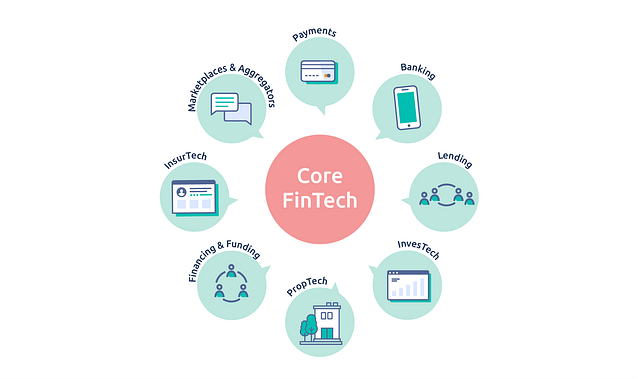

Understanding FinTech Part 1: More “Fin” than “Tech”

Understanding FinTech properly starts with defining exactly what ‘FinTech’ is. FinTechs provide financial services or products (rather than simply engaging in providing technology solutions) to end-users. Thus they are product-focused and typically operate B2C business models. They are “old” in the sense that the products and services FinTech companies provide have been around for decades (if not centuries), but recent developments in technology have opened this frontier to new players and models.

Payments

There was a time not so long ago when banks and credit card companies ruled the world of payments. However, today we pay for more things on mobile devices, people are more open to the idea of online banking, and accept that it is safe. The general public are ready to start really understanding FinTechs, the plus-points they offer and start using them in their daily lives – and at the same time, companies like Stripe, Klarna and Wise are all lining up to challenge the ‘old-school’ payment providers. They claim to meet customer demand for faster, cheaper, and easier-to-use services, and the amount of customers they have has proven that they are obviously succeeding in it, too.

Banking

In addition to innovations in payments, understanding FinTech means comprehending just how much new players such as N26, Revolut and Monese have changed how daily banking activities should work, at a fundamental level. By making it possible to open a mobile UK account without a UK address or credit history, make free international money transfers, and spend money abroad without exchange rate fees, they have made services that did not offer any flexibility in the past obsolete.

Lending

No guide to understanding FinTech would be complete without talking about lending, investing, and trading though. The lending business of banks is facing unprecedented competition from peer-to-peer lending platforms that aim to change the lending and investment landscape. The model’s success lies in its ability to connect borrowers with investors through online marketplaces. These platforms often provide access to credit for people with little or no credit history, opening up possibilities, and contributing to community wellbeing.

InvesTech (Capital Markets and Investing & Trading)

InvesTech was created so investors would not have to deal with large financial institutions in order to access trading platforms, relevant and timely financial information, or charting software – and let them do it in a more flexible and customised way. Whether it’s financial news and information, trading platforms and investing solutions, or social trading and investing, platforms like ScalableCapital and Betterment offer safe, cheap, and easy-to-use ways for investors to control their money, and how it’s being handled.

PropTech

Since the name isn’t quite so clear as ‘InsurTech’ or ‘InvesTech’ here, we’re going to take a detour into ‘understanding FinTech vocabulary’ for a second. Put simply, ‘PropTech’ refers to businesses using technology to change and improve the way we buy, rent, sell, design, construct and manage residential and commercial property. Previously limited to renting or mortgages, now thanks to companies like Wayhome or Point, you can sell small fractions of the equity in your home to investors, and you do not have to just keep living there, but live there as if it were your own home. Meaning, you can re-decorate and design your house the way you want.

Financing & Funding

Owning a small business can be challenging, as accessing capital for your business is a slow and difficult process and you have to spend your days juggling your working capital to pay for projects that help you grow. Companies like BlueVine and Fundbox give their clients access to capital, speed, simplicity, and transparency — no long waits, paperwork, or hidden fees that often come with other financial institutions.

InsurTech

Just as FinTech is transforming the banking world, InsurTech has set its sights on the insurance industry, where it is exploring areas that large insurance firms don’t care about, such as offering social insurance, and using new streams of data from internet-enabled devices in order to price premiums in a dynamic manner. Good examples are companies like Oscar and Lemonade, which have created a different and modern user experience in dealing with an insurance company.

FinTech Marketplaces & Aggregators

The aggregation of financial data has become a great business, because if all the personal and banking data for a given customer is available in a single space, that information becomes easier to use and operations are easier to carry out. FinTech marketplaces such as Raisin, which have an unlimited scale and are not burdened by the constraints of conventional transactional businesses, are thus some of the fastest growing businesses.

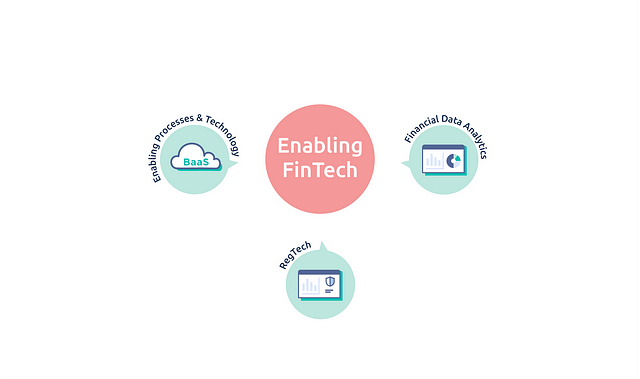

Understanding FinTech Part 2: Enabling FinTech

So far in our guide to understanding FinTech, we’ve seen how companies have used new technologies for innovation. Now we’ll take a closer look at how understanding FinTech and the innovative technologies available to us in the modern day have enabled companies to go beyond merely modifying services, and come up with totally new business models. It’s only a question of time before this list will be as long as (or even longer than) the one above.

Enabling Processes & Technology

Until now, global banking has been described by the complexities of legacy technology, managing global compliance, and legacy bank processes, in turn creating a slow, complex and costly experience for customers. Companies like Railsbank and Solarisbank aim to change that, by letting you build your own banking products using a banking and compliance platform that connects a global network of partner banks with companies that want API access to global banking in order to transact business digitally, and in a compliant way. They’re using BaaS to do that, too.

Like SaaS (Software-as-a-Service), IaaS (Infrastructure-as-a-Service) and PaaS (Platform-as-a-Service), BaaS is an industry-specific service. BaaS platforms provide a cost-effective, easy and fast way for non-banks to launch various financial products by letting you pick the bricks you require, and assemble custom solutions to fit your business needs. On top of that, there’s no need to become a bank and have all the regulatory and compliance responsibilities that banks do.

Financial Data Analytics

Understanding FinTech properly requires us to acknowledge just how vitally important data is to the whole process. That being the case, it is not surprising that the development of machine learning and the growing access to Big Data has resulted in solutions that use data as their core input. Big Data Scoring, a cloud-based credit decision engine, helps banks, telecoms and consumer lenders improve credit quality and acceptance rates through the use of Big Data. Tala, whose credit models allow them to evaluate an applicant’s creditworthiness and capacity using the data on their mobile device, can evaluate and score even those customers who have no formal credit or banking history.

RegTech

Returning to our subsection on ‘understanding FinTech vocabulary’, ‘RegTech’ refers to the use of new technology to facilitate the delivery of regulatory requirements. As the rise in digital products has increased incidences of data breaches, cyber hacks, money laundering and other fraudulent activities, agile regulatory technology that uses tools such as predictive analytics helps large companies better understand and manage their risks. Good examples of this are ComplyAdvantage — the world’s only AI-driven risk database, which predicts the crime risks of people and companies, and Fenergo, an end-to-end Client Lifecycle Management solutions provider.

Conclusion

As said in the beginning, the list above is not by any means conclusive, and so this guide to understanding FinTech covers only the technology’s most widespread uses.. However, there are also very interesting things happening in the areas of accounting, invoicing, working capital management and, of course, cryptocurrencies. Feel free to start exploring on your own – but as alwaysI’m very interested in your thoughts and comments, so shoot!

MOONCASCADE

Mooncascade is an advisory, design, and software development company that guides businesses through the ever-changing digital landscape. Mooncascade’s mission is to help small companies grow and established businesses move quickly.

If you are working within the fast-paced and highly regulated FinTech industry, Mooncascade can apply a wide range of skills and experience to your mobile app development. Whether you need help with scoping a new product, adding a new solution to an existing product lineup, or making sure your back-end set-up can support your new product plans – Mooncascade knows the way.

So, if you have an idea for a great new FinTech product and you need a Product Development partner, then have a look at what we’ve done for FinTech companies, and get in touch!